The most important question in the freight market is when we will reach the bottom. The Cass Freight Index data indicated a worsening trend, but there was optimism for improvement.

The monthly report’s theme is “Bouncing Along the Bottom.” Tim Denoyer of ACT Research said, “The volume downturn appears to be in the later innings,” indicating a potential new cycle for the U.S. freight transportation sector.

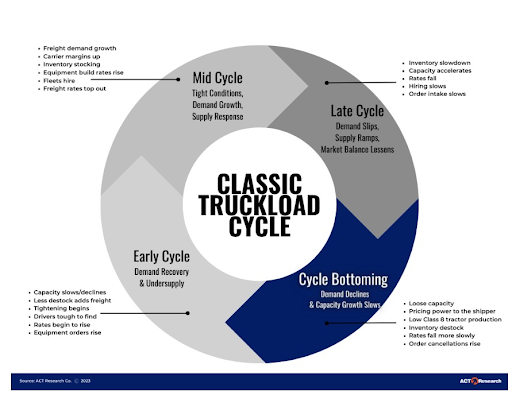

Denoyer, on the other hand, called the current time in the freight business a “cycle bottoming.” In the image that goes with the report, you can see that this cycle has a number of features, such as extra capacity, price pressure for the shipper, a lack of Class 8 tractors, a slower drop in rates, and a rise in rejected orders. The “wheel” for cycle bottoming focuses mainly on the signs of “demand declines and capacity growth slowing.”

Cass Freight Index Shows Continued Decline in Shipments and Prolonged Downcycle in Freight Market

Denoyer stated that the current market is missing one aspect of cycle bottoming, which is the lower level of equipment production. He writes that pressure remains on fleets to seat these tractors as Class 8 build rates remain elevated.

Shipments in the Cass Freight Index decreased by 1.6% from May to June, or 1.9% after adjusting for seasonality.

The measure decreased by 4.7% compared to last year. The yearly rate of change in June was slower than in May, at 5.6%. The shipping index is 12% lower than in December 2021, when the cycle peaked, according to Cass.

The study shows that the current “downcycle” has lasted for 18 months, marking a continuous decline over the years. Cass mentioned that the average length of the last three recessions was 21 to 28 months.

The Cass Freight Index Shows a decline in Spending and rates but Optimism for Future shipping.

According to Denoyer, there is optimism regarding shipments. The reason for this optimism is that although declining real retail sales trends and ongoing stocking are still affecting freight volumes, there is a shift in dynamics due to the improvement in real incomes, and the worst of the destocking is now behind us.

The Cass Index spending fell 2.6% from May to June, and it fell 24.5% from June 2016 to June 2017.

Cass discovered a 1% decrease in interest rates from May to June due to declining exports and spending.

Shipments dropped 1.9% from May, and prices dropped 0.8%. This caused the spending index to drop by 2.8%.

The Cass Truckload Linehaul Index Shows a continued decline in Fuel Spending and the truckload market.

Fuel spending is included in the score. The Cass Truckload Linehaul Index decreased by 0.4% from May to June. It should be less random without gas costs. The drop is smaller than the drop of 2.6% between April and May.

Cass says the average loss in the last two months is 1.5%, which is almost twice as much as the average loss in the six months before at 0.8%. The drop hasn’t slowed down in the last two months.

Cass writes in the report that this index includes both spot and contract freight, serving as a broad truckload market indicator. The larger contract market is expected to continue adjusting down, given the significant decrease in spot rates.

Sales dropped by 4.7%, and other Cass indicators also decreased significantly year over year. The spending index, estimated freight rates, and truckload linehaul index are all down.

The third-quarter bounce of 6.6% would compensate for the drop in the second quarter of 2017 and this year. Tom Nightingale, CEO of AFS, mentioned that truckload prices are stabilizing, but shippers still have an advantage in the market.

The ultimate guide to book dry van dispatch services!

Final Wording

Overall, the Cass study suggests potential benefits for the transport industry. The market is about to start a new cycle, and the current drop is almost over. To know more about trucking and logistics industry daily, check Lading Logistics. We also provide all kind of logistics solutions to businesses.